I wrote a bunch of posts on bitcoin between 2012-2015, but they tailed off a bit in late 2015 and 2016 as my attention turned to other subjects, namely old fashioned banknotes and cash, a terrifically fertile topic. Because my bitcoin posts tended to get a lot of comments at the time, I thought it would be worthwhile to go back and review some of the predictions I made, both for my sake and that of my readers.

My predictions tend to fall into three related buckets.

- Bitcoins will not become a generally-accepted medium of exchange

- Even mainstream organizations like the Fed might one day want to adopt bitcoin tech

- Bitcoin will fall to zero

From a more anecdotal perspective, I live in what I like to think is a fairly vibrant part of Montreal filled with early adopters, but I never see shops or cafes that accept bitcoin. None of my circle of friends and family have ever tried the stuff, and when they ask me about it, it's always to gossip about the crazy high prices—not bitcoin-as-a-medium-of-exchange. Let's face it, bitcoin and other cryptocoins are great speculative vehicles, but they're flops as money.

On the second front, I've written about how the distributed ledger aspect of bitcoin could be split off from the token itself and used by financial institutions See here, for instance. This is the rough idea behind the "blockchain" movement that started up in 2015 or so. We'll see if it pans out. I also predicted that central banks would adopt bitcoin technology before banning it, perhaps in the form of a distributed currency, and have since wrote multiple posts on the Fedcoin idea. No central bank has quite got there yet, but they've all started talking about digital currency and have even been experimenting with it. So I think I've done alright on these predictions.

It's boring being right because you don't learn anything. My last prediction, that bitcoin will hit zero, is my most interesting one because I got it so wrong. In 2012, I wrote:

"My hunch is that bitcoin still has a positive value because proper competition will take a few years to truly develop. Let's see where we are in December 2013."By December 2013, bitcoin had hit $800, not $0. Similarly, this:

"There is no way to arbitrage this premium away directly, but over time competitors will peck away at it, causing bitcoin's price to deteriorate back to its fundamental value, which I'd guess is <$1."Or this from 2014:

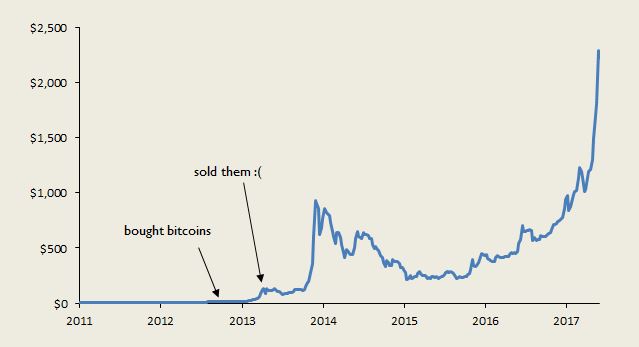

"If I'm right, in the future bitcoin will be a smaller part of the cryptocoin world than it it now, whereas stable-value non-bootsrapped crypto assets, like Ripple IOUs, will be a larger part of that world."To further illustrate how bad I got this one,I once owned 24 bitcoins. I bought them back in the fall of 2012 for around C$12 each (~US$10) for a total outlay of C$290. Thinking I was a genius, I sold out the next year when the price hit C$100, earning what thought to be a nice 700% return. Had I ignored my prediction and held, given today's bitcoin price of ~CAD$3000 my small stash would be worth a cool C$72,000. Ouch. That's not fun to read.

Given this incredibly wide miss, it's high time to re-evaluate my reasoning for a zero price of bitcoin. Do I turtle-in and keep my prediction or do I update it?

---

Here's how I've been thinking about the problem.

There are two types of assets in this world. Type A assets can only provide a return to their current holder if a stream of subsequent investors, buyers, or participants are recruited to provide that return. Examples include Ponzi schemes, chain letters, and pyramid schemes. Type B assets, on the other hand, can provide a return to their owner, even if no subsequent person ever steps forward to acquire that asset. Good examples of Type B assets are gold, land, stocks, and central bank-issued banknotes.

Say a buyer's strike suddenly hits the market for a Type B asset. Everyone decides to sell at the same moment so that the asset is offered at $0. An arbitrage opportunity presents itself. Since this asset will either yield a dividend (in the case of a stock), have some usage in decorating (like gold), or is destined to be repurchased by its issuer at some positive price (think central banks withdrawing banknotes by selling assets), anyone who buys it for $0 is getting something for nothing. As people compete to feast on this free lunch, prices will re-ratchet back up until the opportunity has disappeared. For this reason, Type B assets are characterized by price floors and buyers strikes are not crippling.

No equivalent arbitrage opportunity presents itself when a buyer's strike hits a Type A asset. Say Bernie Madoff issues a bunch of tickets, each providing its holder with a spot in a Ponzi scheme. A few days later, no one wants to purchase Madoff's tickets. Sure, you can now buy a ticket for $0, but because they have no intrinsic value the only way you'll be able to come out ahead is by selling it for more to another buyer, say for $1. This will require that you (or someone else) incur expenses on marketing the scheme i.e converting already angry sellers into buyers. This sounds like an awful lot of work, certainly too much to merit paying anything more than $0. Probably better to start an entirely new Type A asset than try to reboot the failed one. The upshot is that because Type A assets lack an arbitrage mechanism and marketing is costly, buyer's strikes quickly bring the game to an end. There is no floor.

Bitcoin is a Type A asset. It is unconsciously so, there being no Madoff-like evil genius at the centre of the scheme. It just sort of emerged spontaneously.

Like other Type A assets, bitcoin lacks a price floor. When a bitcoin buyer's strike hits, and bids across all the bitcoin exchanges evaporate, a bitcoin held in your wallet is worthless. There is no underlying business that can throw off dividends nor a central issuer that can cancel unwanted tokens. Sure, you can always purchase a bitcoin for $0, but in order to come out ahead you'll have to convince someone to buy it for $10. This means you'll have to regenerate the hype, excitement, and belief that initially spawned a positive bitcoin price. If you're not willing to spend time and money on these efforts, you better hope someone like Andreas Antonopoulos will. Whatever the case, any effort to push bitcoin back into positive territory will be costly.

Given that buyer's strikes are the death knell for Type A assets, it is vital to recruit a constant stream of new buyers to the cause. In bitcoin's case, recruitment has been easy. No Ponzi scheme ever boasted as engaging a mythology as bitcoin, starring the dashing and mysterious Satoshi Nakamoto, a radically decentralized digital currency poised to destroy the existing financial system, and "in math we trust". Because these ideas are so catchy, the mythology has pretty much sold itself—an incredibly cost-effective way of recruiting new participants. Every time bitcoin has experienced a lull in buying and its price has plunged, it has never quite fallen to zero. A batch of new converts, inspired by the latest Andreas Antonopoulos video on YouTube, has always emerged from the woodwork.

While the mythology is strong, it has long since spread into the easy cracks, i.e. libertarians and tech geeks. New target demographics, many of which do not agree with the core philosophy underlying the mythology, won't be so easily convinced to add their bids to the queue. As for Satoshi Nakamoto, he/she is almost ten years old now and getting stale. And one of the core promises of the mythology, the birth of a generally-accepted digital currency, has fallen flat. People are getting jaded.

Luckily, Bitcoin has always had a far more seductive recruiting tool, a rapidly rising price. While the technology and philosophy underlying bitcoin might motivate a few geeks, a 50% price jump is a universal intoxicant. Past returns bring the promise of future returns, waves of new buyers pushing the stuff ever higher. However, this process faces limits. The bigger bitcoin gets, the larger the stream of recruits needed to drive the price higher. At some point its market capitalization will get so large that the population of buyers necessary to keep the ball rolling will be exhausted. And when bitcoin can no longer demonstrate that it offers a superior return, a buyer's strike will hit as everyone rushes to sell at the same time, it's price falling to zero.

So in the end, even though I've been terribly wrong I'm going to stick to my guns on this one. If I'm going to recant my bitcoin-to-zero views, you're going to have to convince me that a Type A asset can last indefinitely. I don't see how. Empirically, we know that Type A assets are precarious, short-lived things. There are no Ponzi or pyramid schemes still running from the 1800s, or the 1920s, or even from 2001. Bernie Madoff's Ponzi scheme, which popped in 2008, may have been the longest running Type A asset ever, it's alleged start date being the early 1970s. That's over thirty years. (Public run pension schemes don't count, since the government can coerce participation). If there is a reason that bitcoin can escape this fate, please explain in the comments section—maybe I'll see the light.

I would count gold as a Type A asset and take it as an example of an asset that has lasted for a long time. It has some intrinsic value, but that's nowhere near the market prices.

ReplyDeleteHi Lassi:

Delete"It has some intrinsic value..."

Then by the definitions I laid out it's a Type B asset. If a buyer's strike breaks out and it falls to $0, it will still have some personal value to its owner, say as jewellery.

I agree with Lassi that Gold is pretty close to type A.

ReplyDeleteOn the point of Bitcoin, it is not void of functionality. Think in terms of the computing power that will now have to be brought to modify or fork the ledger. That makes it useful for timestamping services. Timestamping services themselves may experience a spurt in demand when digital imitations keep getting better. Multisig has interesting corporate governance use cases. A combination of these will keep bitcoin at non-zero values for some time. Whether it will be worth thousands of dollars per coin, I'm not sure really.

"That makes it useful for timestamping services."

DeleteIf bitcoin fall to $0, are the timestamping services provided by a particular bitcoin intrinsically valuable to an individual? Is there an arbitrage play to be made, buying a bitcoin at $0 in order to enjoy, say, $10 worth of time stamping services? The same goes for corporate governance. Does 1 bitcoin in your wallet provide the owner with, say, $10 per year of corporate governance services?

If bitcoin falls to zero or anything close to it its security is gone and you'd be mad to use its blockchain as a basis for any meaningful financial contracts.

Delete1. There were at least two research papers this year concluding that Bitcoin's price volatility is falling and will be at fiat level within a couple of years. In addition to that, I have yet to hear a good argument for why people's demand for a medium of exchange is inversely proportional to volatility, every economist seems to just assert it, or, view it from the point of view of policy rather than demand from actual holder. Except for Austrians, who sometimes argue that people prefer a medium of exchange slowly rising in value.

ReplyDelete2. There is an inherent conflict that public institutions face, on one hand they need people to keep holding fiat money in order for it to keep value, but on the other they need to control its flows and quantity for taxation and policy purposes. Blockchain based central bank money can't solve this dilemma.

3. The price of everything goes to zero over a long enough time, at the latest at the heat death of the universe. The average life expectancy for fiat currency is 27 years. The clock is ticking.

I see no reason to prefer holding fiat to Bitcoin except for short term expenses. Over the many years I have consistently maintained that nobody knows what the price of Bitcoin will be, I said this also in the interviews, I haven't made any price predictions in my papers, and I even said that people claiming to know the future price of Bitcoin are lying.

Hi Peter, long time no see.

DeleteThe specific challenge that I'm putting out in this post is for readers to convince me that a Type A asset can last indefinitely. I noticed that you haven't criticized my Type A/B distinction. Am I to take it that you agree that bitcoin is a type A asset?

"The average life expectancy for fiat currency is 27 years."

Where'd you get that stat? Type B assets like fiat money, stocks, bonds, land and goods can of course become valueless. But not because of buyer's strikes. They become valueless because of competition, fraud, changing tastes, mismanagement, war etc.

"Except for Austrians, who sometimes argue that people prefer a medium of exchange slowly rising in value."

You may be surprised to hear that this is actually standard economic theory... Friedman's optimal quantity of money, or the Friedman rule.

Bank deposit money has a fundamental source of value as deposits can be exchanged for economic resources that borrowers are contractual committed to supply to deposit holders in order to honour their loan contracts. There is no such counterparty in Bitcoin.

DeleteDinero: I'm not really following you. Bank deposits have fundamental value because debts are payable in deposit money?

DeletePeter: Just looking back at old posts. You and me have been going back and forth on this for a while!

http://jpkoning.blogspot.ca/2012/11/bitcoin-for-monetary-economists-why-it.html?showComment=1353264733679#c4342543933011566838

> JP Koning

DeleteThe deposit is created from the loan contract that created it and the loan contract entails that the borrower will sell economic assets to the deposit holder to honour the loan contract, and so the value of the deposit is inherent from the loan contract.

I agree with you JP. Haven't really spoken or thought much about bitcoin for a while but then got into a conversation about it over the weekend and pretty much took the line you give here.

ReplyDeleteWhat's really interesting to me though is to see you use words like 'unconscious' and talk about the power of it's mythology as you try to get to grips with it intellectually. Come over to the dark-side JP (i.e. psychoanalysis and even magical and mythological thinking). It's fun!

Thanks for stopping by, Jonathan. There are a lot of strange things going on with bitcoin (and other monies for that matte, say like the Somali shilling). Not sure if I'd go as far as magic, but mythology is certainly one of the drivers behind the value of these things.

DeleteJP, You make two mistakes in your predictions.

ReplyDeleteFirst, Bitcoin has future value as a means of payment. It's first "payments" use case is money transfers, and is already being used in that capacity. Firms like Coinbase are actively working on consumer apps that should speed retail payments use. The question is not whether it is a payment mechanism today; it's whether it will be so in the future. Speculators buy the currency based on their assigned probability of it coming about. The same is true of Ether, but more so. Ether has a built-in use case. The more businesses are erected on this smart contract platform, the more Ether is required to make their economy run.

Clearly, you get the attractiveness of blockchain technology to facilitate payments. So what is stopping you from seeing the future value of Bitcoin/Ether as an MOE must be...

2) Your second mistake, which is confusing the intrinsic properties of a UOA with its currency exchange volatility. What makes a good UOA is trust in a limited supply and future utility as a MOE. Let's do a thought experiment to show that:

It's Argentina, and the government directs the central bank to print Pesos to finance the ballooning deficit, and it successfully outlaws the USD as a means of payment even in the black market. However, impeachment procedures are proceeding against the president and Vice President, and the next government is expected to back central bank independence and fiscal austerity. You check your Bloomberg to see the USD/ARG exchange rate, and it is highly volatile depending on news of impeachment or money supply. Given this volatility, you conclude that the USD is not a good UOA, and therefore also not a viable future MOE.

What's wrong with the above example? Competing UOA's like the USD can always exhibit current volatility. Speculators will buy it in expectation that it's future MOE value will be higher. That speculation, if it forces the price up, attracts investors that want a store of value and expect the price to continue to rise, and also specific payments use cases like illegal capital flight. These investors/payers become a larger % of owners, and the volatility falls, thus attracting more investors/payers. Eventually, speculative demand falls away and the exchange value becomes more stable.

"First, Bitcoin has future value as a means of payment. It's first "payments" use case is money transfers, and is already being used in that capacity. "

DeleteLet's say bitcoin is going to become more widely adopted as a means of payment, as you predict. That's only a cosmetic change; it's still a Type A asset. After all, the property of being liquid is not intrinsically valuable... it derives from the item's ability to be passed off to the next buyer. Which leads me back to the challenge I posed at the end of my post: convince me that a Type A asset can last indefinitely.

Put differently, if Madoff had managed to make his Ponzi claims more liquid, say by getting people to pass them around like banknotes, do you think his scheme would have been able to continue forever?

"That speculation, if it forces the price up, attracts investors that want a store of value and expect the price to continue to rise."

Perhaps we have different definitions of investing and speculating. Investors buy Type B assets because they expect price to converge up to fundamental value. No investor would buy, say, bitcoin because they are attracted by a recent history of rising prices. I would reword your phrase to say:

"That speculation, if it forces the price up, attracts more speculators that want a store of value and expect the price to continue to rise."

Why do you believe bitcoin is a Type A asset, when it has even more utility than gold, a Type B asset? Every time bitcoin price falls, it's not new entrants that get convinced to buy it up that stabilize the price, it's the old holders who understand its utility and future potential who buy it "cheap," just like with falling stock price of an otherwise solid company.

ReplyDelete"...who buy it "cheap," just like with falling stock price of an otherwise solid company."

DeleteStocks and gold can both get "cheap" relative to some baseline level. In a stock's case, this baseline is its fundamental value, which is driven by the business's ability to generate earnings, while in gold's case the baseline is its value as a commodity, say for gilding or in circuitry. Bitcoin can never get "cheap" because, lacking either fundamental or commodity value, it has no baseline.

But bitcoin does have a whole ecosystem of businesses that work on top of it, from transferring value, to recording messages, to merchants that can't use any other system (gambling and drugs). Their earnings are only possible because of bitcoin's existence. The baseline, like baseline for any currency or money transfer system, is based on how much volume for actual use it has (not just speculation or trading). This use is no different from gold's gilding or circuitry, or a stock's business being able to generate earnings. This is why Bitcoin is absolutely a type B asset, not A, and why a lot of people (especially those still stuck in the "intrinsic value" mindset) have so much trouble understanding it.

DeleteRassa: "The baseline, like baseline for any currency or money transfer system, is based on how much volume for actual use it has (not just speculation or trading)."

DeleteYou can't compare bitcoin to regular currency. The "baseline" for a regular currency like the U.S. dollar is not set by how much volume it has a monetary instrument.

What give the U.S. dollar fundamental value, or a baseline, is the fact that the issuer, the Fed, promises to repurchase and cancel dollar if they fall too fast relative to the Fed' target. This backstop is why regular currency is a Type B asset. If, like the dollar, bitcoin had a central issuer that promised to contract the supply, it would also be a Type B asset, but of course the existence of a central issuer would go against bitcoin's underlying philosophy.

"This use is no different from gold's gilding or circuitry, or a stock's business being able to generate earnings."

Monetary usage is categorically different from gold's gilding or an underlying business's capacity to generate earnings. The value of monetary services depends entirely on future buyers emerging... whereas gold and stocks are valuable for their own sake.

"This is why Bitcoin is absolutely a type B asset, not A..."

If you want to convince me that bitcoin is a Type B asset, you need show me what intrinsic qualities it has such that, in the event that suddenly no one will accept the stuff, it won't fall to zero. Monetary services are certainly valuable, but they are not intrinsic.

I think you're better off yielding me the point that Bitcoin is a Type A asset, but telling me why not all type A assets need fall to zero.

So then isn't gold a Type A asset too? 95% of its value is from speculation and use to transfer and store value, and the remaining 5% could easily be replaced by upcoming advances in carbon fibers and nanotubes. If gold's limited use in electronics is made obsolete, it will crash to zero too, right?

Delete"What give the U.S. dollar fundamental value, or a baseline, is the fact that the issuer, the Fed, promises to repurchase and cancel dollar"

DeleteWith what? Other dollars? This promise has failed to maintain a currency's value in 100% of hospital cases. I don't think USD and EUR will be the exception.

"If, like the dollar, bitcoin had a central issuer that promised to contract the supply, it would also be a Type B asset, but of course the existence of a central issuer would go against bitcoin's underlying philosophy."

But bitcoin DOES have an issuer that promises to contract the money supply. It's the public, unalterable algorithm that continually reduces inflation until inflation stops. The supply may not be reacting to the overall economy (other than though private markets), but it's public and predictable.

"So then isn't gold a Type A asset too? 95% of its value is from speculation and use to transfer and store value, and the remaining 5% could easily be replaced by upcoming advances in carbon fibers and nanotubes."

DeleteGood question. I was careful to set up the Type A vs Type B distinction so that even if an asset's value is determined 95% by speculation, it is still a Type B asset. To be honest, I'm not really sure how much of gold's value is due to speculation.

"If gold's limited use in electronics is made obsolete, it will crash to zero too, right?"

Well it has other applications too like jewellery, dentistry, aeronautics, and medicine. But yes, if these were made obsolete, it would become a Type A asset and eventually crash to 0.

"With what? Other dollars?"

Not with dollars. With bonds that it holds in its vaults. These bonds in turn are backed by the government's ability to tax the population.

"But bitcoin DOES have an issuer that promises to contract the money supply. It's the public, unalterable algorithm that continually reduces inflation until inflation stops."

The protocol is designed to eventually stop making new bitcoins, but it can't outright destroy them, not like a central bank can.

JP,

ReplyDeleteI think your "Type A" fomulation is too loose. There are assets that have zero intrinsic value. A pyramid scheme certificate is a good example. It has no intrinsic usefulness or backing.

So now let's look at Ether. It's possible to set up a whole business model on Ethereum. For instance, the DAO was one (it got hacked, but let's leave that aside). To transact on that platform, one must use Ether as a means of payment. This is a feature of the platform, not an arbitrary add-on. The very nature of tokenized blockchain business models is to use tokens, rather than equities and prices, as incentive signals. Ether is essentially a technological innovation, one that may be as important as equity itself, just as smart contracts may end up being as important as contracts.

Further, I think you confuse the nature of a network effect. Cryptocurrencies follow Metcalf's Law: each additional node adds value exponentially. That does not mean that the nodes need to grow exponentially to support value, as is the case with a pyramid scheme. These are mathematically two very different functions. If Bitcoin reached, say, 50m users, it would not need 51m to keep its value from going to zero. It's 50m users would be a sufficiently large network to have created lasting value as a means of exchange.

Lastly, regarding your speculation vs. investment point: Remember that from a portfolio diversification standpoint, asset price volatility is not a problem. An investor can plan to hold BTC as a store of value even though its price fluctuates wildly. The same is true of gold. They may make the investment anyway due to the assets perceived behavior in certain states of the world. The more speculators raise the price of an asset, the more investors receive a signal that this state of the world is probably. Thus, speculation leads to perceived viability as a store of value, and that perceived viability becomes a self-fulfilling prophecy. Feedback loops are inherent to network dynamics, and this is just one example. If you think prices are ergodic and all actors independent, then you have the makings of a neat math experiment, but not a description of a market :).

"That does not mean that the nodes need to grow exponentially to support value, as is the case with a pyramid scheme. These are mathematically two very different functions. If Bitcoin reached, say, 50m users, it would not need 51m to keep its value from going to zero"

DeleteSo to bring this back to my initial setup of the problem, you seem to be agreeing that bitcoin is a Type A asset and not a Type B asset, but that it somehow escapes the common fate of other Type A assets.

To knock me off my perch, you still need to explain to me how Type A assets survive buyer's strikes. As I said @ 12:35 PM, a Type A asset that gets adopted as a means of payment (say Madoff's certificates become a popular money) is still a Type A asset.

But in order for the Ethereum blockchain to function successfully and reliably as a basis for more complex financial contracts it has to be secure and for it to be secure it has to be prohibitively expensive to manipulate it and for that to be the case Ether has to have a high enough value and for that to happen speculation is necessary.

DeleteSo I think it's kind of putting the cart before the horse to explain the value of the token by referring to all the things one can use its blockchain for. The token has to have value before all those things can actually be done. And that is where speculation comes in. Speculation is what gives the token value and hence what makes the applications on the basis of its blockchain possible.

JP,

DeleteLet's stick to a narrower point of contention. As I understand it, you believe Bitcoin is a Ponzi scheme. A Ponzi instrument ha s value only if the participants in the scheme expand exponentially. This is not true of Bitcoin. Ergo, Bitcoin is not a Ponzi scheme.

Further, as I've said, both Bitcoin and Etherderive their value from speculation over their future JOE status. Speculators at least in part are willing to bet on the fact that they are technologically superior payment platforms. This is simply not a quality of Madoff certificates.

Diego,

Delete"As I understand it, you believe Bitcoin is a Ponzi scheme."

I think I'm being more nuanced than that. I said it was a Type A asset. My definition of a Type A asset doesn't require that participation expand exponentially for it to have value, although some Type A assets like ponzis have this quality.

While Ponzi schemes emerge from deceit, bitcoins emerge from electric energy. Grouping them in the same asset type is disingenuous. I'm skeptical of the idea of "intrinsic value" but it's insightful to explore its opposite: "extrinsic value." If any 'thing' has value it is food (in the case of animals) or light (in the case of plants), or energy (in the general case.) Wait a minute....

ReplyDeleteHi Alex,

Delete"While Ponzi schemes emerge from deceit, bitcoins emerge from electric energy. Grouping them in the same asset type is disingenuous."

I granted in my piece that bitcoin has no "Madoff-like" genius at its centre. See fifth or sixth paragraph from the bottom.

In my post I am putting bitcoin and Ponzi schemes in the same bucket because, unlike Type B assets, they both require a constant stream of new buyers to uphold their value. And since Type A assets always fall to 0, so will bitcoin.

To get me out of my intellectual rut, you'll have to: 1) show me that bitcoin doesn't require a stream of new buyers and therefore that it is not a Type B asset; or 2) explain to me why not all Type B assets need to fall to zero. Telling me that bitcoin isn't a Type B asset because it doesn't emerge from deceit is breaking the rules.

"unlike Type B assets, they both require a constant stream of new buyers to uphold their value."

DeleteBitcoin doesn't require a constant stream of new buyers to uphold it's value though. If there were no new buyers, its price would simply remain the same, at the baseline of the economy it currently supports (money transfers between people who can't use other systems, and it being used for its other many uses), not drop to zero. For example, someone will do have to buy it in order to send it to a merchant, and a merchant will still have to sell it to pay his bills.

yep

DeleteThe money transfer utility does sound like some Type B characteristic.

DeleteA competition between those who refuse to accept losses and those burned enough by them to forego it. Still many gamble even though the expected gain is negative and some may consider themselves the house. Not much collector value though.

ReplyDelete"At some point its market capitalization will get so large that the population of buyers necessary to keep the ball rolling will be exhausted"

ReplyDeletePretty much everything you wrote up until this point is correct. Bitcoin is a type A asset AND it has no intrinsic value and therefore is without a >0 price floor AND it sees only very limited use as a medium of exchange.

So as an investment vehicle it stops being attractive at the point when people think not enough new users will sign up to sustain an increasing price.

But the idea at least is that bitcoin gradually evolves from a speculative investment dependent on an increasing user base to a stable store of value (like gold) and/or medium of exchange with a stabilizing price as the increase in new users levels off. As a speculative investment bitcoin needs the prospect of price increases, as a store of value and/or medium of exchange it does not. And the idea (and at least theoretical possibility) is that it transitions from the former into the latter.

This is what makes it different from the examples of type A assets that you mention.

---

What I find surprising btw is that as one of the foremost thinkers on moneyness (and one I learned a lot from in that respect) you insist in the necessity of a >0 price floor and hence on some intrinsic value for something to work as a (non-government) money.

All moneyness is bubbliness.

An asset's value = value it derives from non-monetary uses ('intrinsic value') + value it derives from monetary uses (moneyness). And the extra value that moneyness adds to an asset does not depend on whether that asset's other uses give it a 0 or >0 value. If asset 1 is worth $1 for its non-monetary uses and $2 extra for its monetary use and asset 2 $0 for its non-monetary uses and $2 for its monetary use, for the holder of these assets why would it be worse if asset 2 drops from $2 to $0 when its moneyness is lost than if asset 1 drops from $3 to $1 when its moneyness is lost?

Hi Koen, great points.

DeleteFor others, here is a post Koen once wrote on the topic of bitcoin vs ponzis.

https://philosophyofbitcoin.blogspot.ca/2014/03/dear-nouriel-roubini-heres-why-bitcoin.html

"In the process of bitcoin's monetization (i.e. as it gradually becomes a universally accepted medium of exchange, and an appreciating or stable store of value) it gradually changes from a speculative investment with a high risk and high ROI to a stable money with a low risk and a low to zero ROI."

I'll grant you the possibility that bitcoin can transition from being a speculative investment to a generally-accepted medium of exchange. If so, people no longer hold it in the expectation of passing it off to a speculator, but because they expect to pass it off to a store keeper or to pay a debt. In which case the public might be happier with a flat bitcoin price, as you point out.

All assets, including liquid ones like central bank money, suffer from temporary excesses of supply, or what I've called buyers' strikes. The price of these assets typically falls until buyers are lured back into the market. What lures them back is that they can be purchased at less than their intrinsic value. In the case of central bank money, intrinsic value is set by the central bank's threat to sell assets and cancel currency. When money was gold coins, it was the promise of melting down those coins and turning them into jewellery that lured people back.

Even if it has succeeded in becoming a popular medium of exchange, temporary excesses in the supply of bitcoin are handled differently than gold coins and central bank money. When everyone tries to get rid of their inventories, new participants who are willing to hold the stuff need to be found. But there is no intrinsic value to serve as a motivator. Bitcoin's price could fall very fast, maybe to zero, before the next batch of buyers ever materializes.

This means that even if bitcoin has become a popular money, it could be highly volatile, and this paradoxically militates against it ever becoming a popular money.

"If asset 1 is worth $1 for its non-monetary uses and $2 extra for its monetary use and asset 2 $0 for its non-monetary uses and $2 for its monetary use, for the holder of these assets why would it be worse if asset 2 drops from $2 to $0 when its moneyness is lost than if asset 1 drops from $3 to $1 when its moneyness is lost?"

...let's further assume for simplicity's sake that they will each stay at their end prices ($1 for asset 1 and $0 for asset $2) forever? I'd say that a $2 loss is just as bad as a $2 loss.

Normally, the extra value that moneyness adds to an asset is quite small, or at least that's how I see it. Maybe 2% of the value of a Google share could be attributed to moneyness? When gold coins were money, a coin might be worth a few percent more than its value as bullion? Bitcoin is interesting because not only is the contribution made by its moneyness quite large, but it may even have no intrinsic component at all--it is pure moneyness.

Thanks for your reply and for the fact that you so frequently, diligently and thoughtfully respond to people's comments in general.

DeleteLonger response to follow.

"I'll grant you the possibility that bitcoin can transition from being a speculative investment to a generally-accepted medium of exchange. If so, people no longer hold it in the expectation of passing it off to a speculator, but because they expect to pass it off to a store keeper or to pay a debt. In which case the public might be happier with a flat bitcoin price, as you point out.

DeleteAll assets, including liquid ones like central bank money, suffer from temporary excesses of supply, or what I've called buyers' strikes. The price of these assets typically falls until buyers are lured back into the market. What lures them back is that they can be purchased at less than their intrinsic value.”

This I don’t understand. It seems to me that what lures a buyer back is the prospect of being able to sell the asset later for more than she has to pay for it now (discounted for etc). The price of the asset currently being below the price solely based on its non-monetary value is one way of satisfying that condition. But it’s not the only one.

The simple speculation that the asset will be worth more in the future (probability*expected future value) is another way of satisfying the condition.

And while something with zero non-monetary value would not be able to satisfy the condition you stipulated (unless there are ways of buying it at <$0 and/or selling it at >$0) it would at least theoretically be able to satisfy that speculation condition. It always makes sense for me to buy bitcoin at whatever cost if that cost is lower than what I think the probability*expected future value is.

And everybody else should think the same way.

“In the case of central bank money, intrinsic value is set by the central bank's threat to sell assets and cancel currency. When money was gold coins, it was the promise of melting down those coins and turning them into jewellery that lured people back.”

Yes, these are ways of providing a >$0 floor.

“Even if it has succeeded in becoming a popular medium of exchange, temporary excesses in the supply of bitcoin are handled differently than gold coins and central bank money. When everyone tries to get rid of their inventories, new participants who are willing to hold the stuff need to be found. But there is no intrinsic value to serve as a motivator. Bitcoin's price could fall very fast, maybe to zero, before the next batch of buyers ever materializes.”

DeleteYes, but as I mentioned above, simple speculation can motivate a buyer in the absence of a currently-below-intrinsic-value-price. And simple speculation is what has driven the price of bitcoin so far anyway, so that may be a reason to think my mechanism is not unrealistic.

“This means that even if bitcoin has become a popular money, it could be highly volatile, and this paradoxically militates against it ever becoming a popular money.”

See above, but to be sure there is a way in which it is necessarily true that bitcoin is more volatile than assets with both monetary and non-monetary roles. Suppose:

1) an asset A has a non-monetary use that is worth $10 and a monetary use that is worth $5,

2) an asset B that has no non-monetary use and is worth $5,

3) monetary value is more volatile than non-monetary value

4) the volatility of the monetary value is the same in both assets

then it is necessarily true that asset B’s total value is more volatile than asset A’s total value.

Besides the question whether assumptions 3 and in particular 4 hold in real life, I am not sure how important this result is for the question whether bitcoin can succeed as a widely used medium of exchange and/or store of value.

"...let's further assume for simplicity's sake that they will each stay at their end prices ($1 for asset 1 and $0 for asset $2) forever? I'd say that a $2 loss is just as bad as a $2 loss.

Normally, the extra value that moneyness adds to an asset is quite small, or at least that's how I see it. Maybe 2% of the value of a Google share could be attributed to moneyness? When gold coins were money, a coin might be worth a few percent more than its value as bullion? Bitcoin is interesting because not only is the contribution made by its moneyness quite large, but it may even have no intrinsic component at all--it is pure moneyness.”

Yes to all, and yet our conclusions differ. So our main point of difference seems to be whether speculation could also motivate a buyer in the buyers’ strike scenario you sketch.

(and I would still *love * to see a bitcoin ad campaign with your slogan “Bitcoin: Pure moneyness”)

I wrote:

Delete"This I don’t understand. It seems to me that what lures a buyer back is the prospect of being able to sell the asset later for more than she has to pay for it now (discounted for etc). The price of the asset currently being below the price solely based on its non-monetary value is one way of satisfying that condition. But it’s not the only one.

The simple speculation that the asset will be worth more in the future (probability*expected future value) is another way of satisfying the condition."

But to be sure, this would be as long as bitcoin still has room to grow. Once it is transitioning into a stable store of value and/or medium of exchange a buyer would be motivated not by speculative gains but by its utility as a stable store of value and/or as a medium of exchange.

Having said that, in case of a hypothetical buyers' strike there would by definition still be room to grow (again) and hence a speculation motive for buyers.

Koen,

Delete"This I don’t understand. It seems to me that what lures a buyer back is the prospect of being able to sell the asset later for more than she has to pay for it now (discounted for etc). The price of the asset currently being below the price solely based on its non-monetary value is one way of satisfying that condition. But it’s not the only one.

The simple speculation that the asset will be worth more in the future (probability*expected future value) is another way of satisfying the condition."

So you're saying that if something is a Type A asset (or even a Type B asset made up of 50% moneyness), and it begins to fall in value, say from $x to $y, then people don't need some notion of "fundamental" or non-monetary value to re-enter the market as a buyer. They might just use a trader's rule of thumb that tells them that someone else is likely to once again pay $x for the asset a few months later, so buying at $y will lead to a sure profit. And with enough people using the same rule of thumb, the Type A asset will never fall to $0. It will rise back to $x.

That could certainly occur. And as you point out, this seems to have driven the price of bitcoin so far. But why should everybody else think the same way about the asset's future value, as you later claim?

There might be another trader's rule of thumb that says the opposite i.e. the trend has turned and in falling to $y an important support line has been breached, so the price should go down to $z. And if enough people act on this second rule of thumb they will cancel out the effect of all those speculators basing their trading on the first rule of thumb. We might even get a cascade effect where the first set of speculators are more-than-cancelled out, the resulting price decline setting off a third trader's rule that encourages people to sell, leading to an even lower price and more selling etc. A buyer's strike.

It is possible that the first trader's rule of thumb works for a long time, but there is no "force of nature" that dictates it must always work. At some point it will stop working. Fundamental value, however, is a force of nature. It never stops working. It will always lure people back into the market.

"There might be another trader's rule of thumb that says the opposite i.e. the trend has turned and in falling to $y an important support line has been breached, so the price should go down to $z. And if enough people act on this second rule of thumb they will cancel out the effect of all those speculators basing their trading on the first rule of thumb. We might even get a cascade effect where the first set of speculators are more-than-cancelled out, the resulting price decline setting off a third trader's rule that encourages people to sell, leading to an even lower price and more selling etc. A buyer's strike."

DeleteYes, this is entirely possible and not at all unlikely.

"It is possible that the first trader's rule of thumb works for a long time, but there is no "force of nature" that dictates it must always work."

No doubt.

"At some point it will stop working. "

You made a bit of a leap there. The fact that it is entirely possible doesn't mean it *will* happen.

"Fundamental value, however, is a force of nature. It never stops working. It will always lure people back into the market."

But to what market? The market for the asset in its non-monetary role or the market for the asset in its monetary role?

We are talking about the latter but why would the asset's non-monetary role lure the buyer back into the market for its monetary role?

The situation seems to be the same for an asset that has no non-monetary role and an asset that does have a non-monetary role. What matters is whether the buyer is lured back into the market for its monetary role. And with the mechanism you describe having a non-monetary role offers no advantage in that regard.

"But to what market? The market for the asset in its non-monetary role or the market for the asset in its monetary role?

DeleteWe are talking about the latter but why would the asset's non-monetary role lure the buyer back into the market for its monetary role? "

People are lured back into a falling market because they want to hold the asset for its non-monetary role. And they do so because the market is pricing that asset below its non-monetary value. These people, who are engaging in a sort of arbitrage (i.e. this is a force of nature), are consumers or value investors. Their buying props up the asset's price, serving as a platform off of which non-monetary value can be re-established.

You need this class of participants to establish a platform. Speculators are trend followers, they typically don't buy assets that are plunging in value. And for those who want to hold liquid media of exchange, they don't like volatility.

Thanks for another reply, JP.

Delete"People are lured back into a falling market because they want to hold the asset for its non-monetary role. And they do so because the market is pricing that asset below its non-monetary value. These people, who are engaging in a sort of arbitrage (i.e. this is a force of nature), are consumers or value investors. Their buying props up the asset's price, serving as a platform off of which non-monetary value can be re-established.

You need this class of participants to establish a platform. Speculators are trend followers, they typically don't buy assets that are plunging in value. And for those who want to hold liquid media of exchange, they don't like volatility."

Maybe I misunderstand you here but this seems to portray speculators as quite dumb. Or dumber than the consumers and value investors anyway.

They apparently don't realize that the reason the asset's price is going up is because consumers and value investors are buying it because it had been priced lower than justified by its non-monetary value.

To the extent that the speculators drive up the price beyond that justified by the non-monetary role they are apparently simply mistaken (they mistakenly think the non-monetary value justifies the higher price) or they set in motion a bubble in a way that is structurally similar to the case of a $0 non-monetary value gaining a positive monetary value (e.g. bitcoin).

In the former it is in any case difficult to see how sustainable non-monetary value can be created in such an accidental way if there are no speculators buying because they expect the asset to gain monetary value in the future.

"Maybe I misunderstand you here but this seems to portray speculators as quite dumb. Or dumber than the consumers and value investors anyway. "

DeleteNot sure if you've ever traded futures, but there is an interesting report issued by the CFTC called the COT report, or commitment of traders. It disaggregates holdings between small speculators, large speculators, and commercials (i.e. hedgers, producers, refiners).

Here it is for corn.

https://www.barchart.com/futures/commitment-of-traders#/technical-charts/ZC*0

You'll see that the line "Non-Commercials or Large Speculators, consisting of Managed Money and Other Reportables (Green Line)" generally moves with the price. Speculators add to their positions as price increases, and go short only as it falls. Commercials (who tend to value the stuff for its non-monetary value) do the exact opposite. Price peaks coincide with maximum spec long positions, valleys coincide with max spec short positions.

We could argue whether the same principle that govern corn markets apply to bitcoin. But a number of other futures market that I've traded like gold, wheat, silver, and orange juice tend to demonstrate this same feature, so I think it is fair to generalize this observation to a broad variety of markets. I don't think speculators are dumb, but I don't think they can be counted to provide much buying support as prices fall. They are trend followers.

"a number of other futures market that I've traded like gold, wheat, silver, and orange juice tend to demonstrate this same feature, so I think it is fair to generalize this observation to a broad variety of markets."

DeleteInteresting point, thanks. I simply don't know nearly enough about the topic to know what to do with this info. It kinda seems that if this is a pattern it would be exploitable somehow (if the info who are buying at a given point is available in that moment), but I don't know. Maybe not.

"We could argue whether the same principle that govern corn markets apply to bitcoin."

Or e.g. markets for art, fine wines, but also gold. More generally, markets where the actual price of an asset seems almost always considerably higher than seems justified (though we disagree about that (I wrote more about this issue in my blog post)) by the asset's non-monetary role.

"I don't think speculators are dumb, but I don't think they can be counted to provide much buying support as prices fall. They are trend followers."

And yet, in the case of bitcoin etc there has always been *something* that stopped a selling trend. Who would that have been if not speculators, given that bitcoin has no non-monetary value. The fact that so far there has always been something that has stopped a selling trend does of course not mean that it will continue to be true in the future. But it does mean that within a finite time period a plunge to zero is not inevitable.

Bitcoin does have some useful purposes for some, mainly escaping capital controls in China and organized crime. Maybe they are not the most ethical of all activities, but bitcoin does provide a useful service for these people. That's why I don't see the price dropping to zero unless those find a better way to send and receive money, or the government finds an efficient way to crack down on bitcoin.

ReplyDeleteI can see that the vast majority getting disappointed with bitcoin and abandoning the idea of new digital money, but as long as bitcoin remains 1) decentralized 2) somewhat anonymous 3) scarce, it will hold the potential to be used as currency for all activities any State don't want you to do.

"Bitcoin does have some useful purposes for some, mainly escaping capital controls in China and organized crime."

DeleteI agree. But those services depend on someone else purchasing the bitcoin. To be a type B asset, bitcoin needs to yield services that are not dependent on another person buying it down the road.

I want to echo Koen's arguments, which I think are correct and also want to highlight that you write "bitcoin could transition from a speculative investment to a medium of exchange". It is the store of value function of a monetary good that is by far the most important function of the three functions money can have (medium of exchange, store of value, unit of account). It's entirely conceivable that in an economy most exchange happens with one good and most savings happens in another (e.g., you can imagine that in Argentina most people trade with pesos but try to save in dollars, which they have a higher trust in).

ReplyDeleteGold currently trades at about $1300 but its use value for jewelry and other things probably only explains at most a few hundred of this price. Gold is mostly "moneyness" or "bubbliness" as Koen writes. Bitcoin is pure moneyness. Silver is a mixture of both and oil is mostly use value. But the fact that gold's use value is, say, $200 is irrelevant to the price it has as a store of value. If tomorrow people in India decided they preferred jewelry in copper or silver, this wouldn't mean the price of gold would crash to zero, or that this would even be likely.

The store of value function of a monetary good comes from people's belief that it will continue to maintain or increase in value over time. This is a game theoretic phenomena because the optimal store of value is the one that every holds their savings in. The nash equilibrium is for a single store of value. The use value isn't what plays into the price of such goods. What is happening is people trying to anticipate which good everyone else will want to hold their savings in. Such goods as very poorly understood because they don't have easy cash flow analysis to obtain a valuation. These goods are "path dependent". That is, the price yesterday and the day before and so on plays a role in the market psychology of where it's "cheap" or "expensive". I.e., its value is entirely subjective. Is gold cheap? Is it expensive? This question has very little to do with its use demand. If gold were to drop to $900 many people would consider it cheap simply because it was $1300 yesterday. Path dependency confounds so many economists because they're much more comfortable with dealing with cash flow valuations.

'Gold currently trades at about $1300 but its use value for jewelry and other things probably only explains at most a few hundred of this price.'

DeleteWhen it comes to use value / non-monetary value there is an important distinction gold's industrial use value and its use value as jewelry etc. The latter is fundamentally dependent on its monetary role while the former isn't. To put it simplistically: Gold is used as jewelry because it's valuable, not the other way around.

Vijay,

Delete"Gold currently trades at about $1300 but its use value for jewelry and other things probably only explains at most a few hundred of this price.

Could be. I don't claim to know how much of the value of gold comes from its fundamental value and how much from its non-fundamental value. But it's certainly a Type B asset.

"The use value isn't what plays into the price of such goods. What is happening is people trying to anticipate which good everyone else will want to hold their savings in. Such goods as very poorly understood because they don't have easy cash flow analysis to obtain a valuation."

The fundamental analysis that convinces buyers to enter the gold market is easy to understand. Gold is a direct competitor with other metals in many industrial and consumer applications, and when it falls below a certain value, it will become cheaper to fashion that product--say a circuit--with more gold than the alternative. At which point a simple profit and loss calculation dictates buying at $900. So I disagree with you. Whether gold is "cheap" or not is a question that can be easily answered by those who only value gold for its use-value.

This is where I think you are fundamentally wrong. Only a fraction of the gold in use is used industrially:

Deletehttps://en.wikipedia.org/wiki/Gold_reserve#IMF_holdings

(about 12% according to wiki). The rest is held in reserve. I.e., either by central banks, in bullion privately, or in jewelry. Jewelry is just another form of "store of value", especially for people in India. I think I was mistaken to lump usage in jewelry as "use value". So I would contend that if the industrial usage of gold disappeared or was supplanted by something else, the value of gold would continue to be much higher than zero.

Let's assume you're right about jewellery.

DeleteThe larger issue is this: can an asset remain relatively close to its fundamental value when an analysis of that asset's distribution shows that most people are holding it simply to sell in the future? I don't see why not. For instance, I can find financial assets that stay very close to fundamental value even though most people who are holding are doing so for speculative motives.

(If you're interested in finance, the argument I'm making is similar to the one made against one of the more common criticisms of passive investing... that once x% of the market invests passively, stock prices will unwind from their fundamental value and no longer have good signalling power. If I recall correctly, someone wrote a paper that says that only a small percent of market participants need to be investing actively for the market to be efficient).

Thanks for your thoughtful replies JP. As a quick aside I found it interesting to discover today that Satoshi Nakamoto had basically the same perspective as Koen and I. See quote below. The essence I think is that first value comes from scarcity (fungibility/verifiability help too). After that the value is almost completely game theoretic and path dependent. For a commodity like gold, its rather trivial use value can get it to "take off" so to speak, but the altitude it reaches after that has basically nothing to do with how it took off.

Deletehttp://satoshi.nakamotoinstitute.org/posts/bitcointalk/428/#selection-21.3-51.70

As a thought experiment, imagine there was a base metal as scarce as gold but with the following properties:

- boring grey in colour

- not a good conductor of electricity

- not particularly strong, but not ductile or easily malleable either

- not useful for any practical or ornamental purpose

and one special, magical property:

- can be transported over a communications channel

If it somehow acquired any value at all for whatever reason, then anyone wanting to transfer wealth over a long distance could buy some, transmit it, and have the recipient sell it.

Maybe it could get an initial value circularly as you've suggested, by people foreseeing its potential usefulness for exchange. (I would definitely want some) Maybe collectors, any random reason could spark it.

I think the traditional qualifications for money were written with the assumption that there are so many competing objects in the world that are scarce, an object with the automatic bootstrap of intrinsic value will surely win out over those without intrinsic value. But if there were nothing in the world with intrinsic value that could be used as money, only scarce but no intrinsic value, I think people would still take up something.

(I'm using the word scarce here to only mean limited potential supply)

"The larger issue is this: can an asset remain relatively close to its fundamental value when an analysis of that asset's distribution shows that most people are holding it simply to sell in the future? I don't see why not. For instance, I can find financial assets that stay very close to fundamental value even though most people who are holding are doing so for speculative motives. "

DeleteI think it's possible too (and the analogy you make with passive investing is an intriguing one). And I think it's also possible that on the basis of the demand by people holding it to sell in the future an asset's value goes and stays much higher than justified by its non-monetary use alone. Bubbles are real and some bubbles are sustainable.

btw, I realize now that we don't mean the same thing by moneyness. For you it concerns only the degree to which an asset functions as a medium of exchange (its liquidity premium) while for me (and I think Vijay) it also includes its function as a store of value (though the exact nature of the causal and conceptual relations between these two functions is not very clear to me at this point).

Moneyness being bubbliness may make more sense in the latter than in the former conception of moneyness. Bubbliness essentially comes down to the game-theoretic mechanism Vijay described. Something has bubble value when people value it for no other reason than that they expect other people to value it (at a sufficiently high level) in the future. Bubbliness is bootstrapping and possibly sustaining a store of value function out of thin air. This can happen either as something added to an already valuable asset or as an asset’s sole value.

Some unclear and freewheeling thinking on explaining the store of value function and its relation to the medium of exchange function:

DeleteWith assets such as works of art, old wines, old coins etc the same game-theoretic mechanism is at play but embedded in a context of social, cultural, aesthetic, epistemic norms, traditions, values, practices and narratives that explain, contribute to, justify or rationalize the value that is stored. The store of value function of an original Rembrandt is ultimately based on the expectation of the buyer that he can sell it later at a sufficiently high price.

This expectation is embedded in and justified by its aesthetic value (as described and argued for by experts), its place in history, in both a historical and art historical narrative, its uniqueness (collectible value) etc.

So these help drive the necessary game-theoretic mechanism (expectations of future value) that is responsible for its store of value function.

The store of value function of a bitcoin on the other hand seems more nakedly based in or constituted by that game-theoretic mechanism alone. It is less obvious how bitcoin was embedded in aesthetic, social, cultural norms, values, practices that explain or rationalize its value and hence justify the expectation of sufficiently high value in the future that its bootstrapping success depended on and that it will need to survive and grow.

(But such things did play some role (e.g. libertarian idealism, subversiveness, beauty of the concept etc) and may continue to evolve to further embed bitcoin in social, cultural, aesthetic contexts and help it to grow further and sustain it.)

Maybe another such context is that of market practices, in the form of bitcoin’s role as a medium of exchange. While typically the store of value function of bitcoin is explained by its current and expected future medium of exchange function, maybe bitcoin’s use as a medium of exchange is better seen as more on a par with the cultural etc factors mentioned above in the context of explaining the store of value function of works of art.

So then it would be not so much the overriding, determining factor that explains its store of value function (as how I think you see it) but one of the elements that embed bitcoin and help fuel and sustain the primary game-theoretic mechanism responsible for its store of value function.

"btw, I realize now that we don't mean the same thing by moneyness. For you it concerns only the degree to which an asset functions as a medium of exchange (its liquidity premium) while for me (and I think Vijay) it also includes its function as a store of value (though the exact nature of the causal and conceptual relations between these two functions is not very clear to me at this point). "

DeleteNo, I believe we have the same definition. I think of it as that extra value that an individual ascribes to a good because they expect that someone will accept it in the future. Whether that person is expected to do so at a higher price (i.e. the motives are speculative) or at the same price ( i.e. the motives are monetary) doesn't matter.

More later. Am having problems keeping up with the pace here given other duties.

"No, I believe we have the same definition. I think of it as that extra value that an individual ascribes to a good because they expect that someone will accept it in the future. Whether that person is expected to do so at a higher price (i.e. the motives are speculative) or at the same price ( i.e. the motives are monetary) doesn't matter."

DeleteThis is probably a good point. Will have to think about it some more.

"More later. Am having problems keeping up with the pace here given other duties."

Serves you right for posting about bitcoin!

;-)

Vijay, great quote. I tweeted it out yesterday.

Delete"and one special, magical property:

- can be transported over a communications channel"

Maybe I am jaded, but I don't transportation over a communications channel a being magical.

We have been developing new ways to circulate value for millenia. Metal --> coins --> paper --> book-entry --> digital-->crypto

I don't see why the next technological development in this chain suddenly means we can escape from what Nakamoto calls the "traditional qualifications for money."

The really magical part is not that it can be transmitted electronically; it's that it can be transmitted electronically without requiring trusting a third party. *That* is what's world changing. It's a solution to a long standing problem of computer science that many thought was unsolvable. And allows something that has literally never been possible in the history of the world (transmission of value at great distance without trust).

DeleteKoen,

DeleteThe Rembrandt is an interesting example. You mention the "cultural narratives" that go into rationalizing why a buyer might "sell it later at a sufficiently high price." I think these narratives explain why we should get a special feeling looking at a Rembrandt in the first place i.e. why has value apart from our ability to sell it, or non-monetary value. National galleries, for instance, are not in the game of re-selling art to the highest bidder... they value a painting for its ability to throw off a repeated stream of consumptive enjoyment to museum visitors. Any improvement in the underlying cultural narrative--say a famous art critic writes a new Rembrandt book--only boosts the expected stream of consumption, and thus the painting's price.

Speculators can of course base their purchases on the fact that they think the narrative justifying a certain Rembrandt is about to get some sort of boost. But in the end the are front-running what they anticipate to be an improvement in the feeling of consuming a Rembrandt (or, taken to the next degree, they are anticipating someone anticipating an improvement in the consumptive experience, this being the game-theoretic stuff you and Vijay are talking about).

I'm skeptical whether the cultural narrative approach can explain bitcoin's valuation. See our discussion on twitter:

https://twitter.com/KoenSwinkels/status/869626386427805696

With a Rembrandt, there is a discrete "thing" to enjoy. You can't just buy 0.001 of a Rembrandt. With bitcoin, what constitutes owning enough bitcoin to be able to feel what the narrative tells us to feel? If 0.00001 is enough, and there are 5 billion people in the world, then there is only demand for 5000 bitcoins.

Preliminary yet belated thought re our twitter discussion: maybe the analogue of the originality aspect of the Rembrandt (vis-a-vis copies) is (also?) the originality of Bitcoin vis-a-vis other blockchains (or new networks running same software as Bitcoin).

DeleteAnyone can copy the existing bitcoin software and start a new bitcoin network, 'just as' anybody can copy a Rembrandt. But others won't value it because it's not the original.

---

and to be sure, my point was that the cultural narrative plays a much more derivative role in the store of value function of bitcoin as opposed to the same function in the case of works of art. To exaggerate, with bitcoin it is much more the naked game-theoretic mechanism at play and all the rest is dress-up

---

More to come (he said forebodingly)

I'm very excited to see your thoughts/responses to Koen's blog post on this topic (which I think is excellent), JP.

DeleteI temporarily took it down and will publish a revised version later tonight.

Deleterevised version is up https://philosophyofbitcoin.blogspot.ca/2017/06/bitcoin-culture-and-value.html

DeleteWhat about if you had a Type A asset, but there was a structural reason why you couldn't have a buyer's strike, i.e. there was a permanent need among some people to make censorship free transactions? If Bitcoin is the best digital currency to make these transactions -- by dint of having the largest market cap and the deepest, most liquid pool -- would that change your assessment?

ReplyDelete"i.e. there was a permanent need among some people to make censorship free transactions?"

DeleteI don't think your example is sufficient to assume away buyer's strikes. Even if there is a set of people who must make censorship free transactions, and a Type A object is the only way to do so, at some point a situation will arise in which--by sheer chance--most of them are sellers of the Type A object, say because they all want to buy some illicit good at the same time.

Hello JP ,

ReplyDeleteI've been following this issue for awhile now. I, along with entire world, find it quite interesting. Also, as most of people here, I'm speculating on digital currencies mostly for fun. That's partially, the reason I'm here, but I'm also an economics student who is naturally curious.

"To get me out of my intellectual rut, you'll have to: 1) show me that bitcoin doesn't require a stream of new buyers and therefore that it is not a Type B asset; or 2) explain to me why not all Type B assets need to fall to zero. Telling me that bitcoin isn't a Type B asset because it doesn't emerge from deceit is breaking the rules."

I've seen the Internet has influenced political elections, and I feel it is likely doing the same with our monetary system. I've seen 6000 websites which promote bitcoin.

Bitcoin may be a ponzi scheme, that needs a constant supply of buyers, and yet the dollar also needs a constant supply of dollars. For all the talk of decentralization, I feel that most decentralized currencies are hoping banks and governments buy them.

I read a bloomberg view article that states that russia is looking to invest in ethereum. According to the article, Russia has failed in technological innovation, and as their oil is running out, they are looking for a technological boost.

I have a feeling that digital/ decentralized currencies could potentially help developing economies, and it could boost a technological revolution in our economy. However, I'm not sure it is worth the cost of disruption.

What are your thoughts?

--adam

Hi Adam, thanks for your thoughts.

Delete"I have a feeling that digital/ decentralized currencies could potentially help developing economies, and it could boost a technological revolution in our economy."

I think mobile money has already had a big effect in places like Kenya, Angola, India, and elsewhere, far more than cryptocurrencies. Because mobile money is stable, and crypto isn't, mobile money will continue to be far more effective in helping developing countries than crypto.

Hi JP, interesting stuff. With this division of A and B assets all networking software must be type A assets. The utility comes from the network effect. So if you devide assets based on the utility at the individual level it will appear that network tools have no intrinsic value. If me and my friends open a joint account at Bernies we as a group still have a Type A asset. But if we own Bitcoins and there are no bids outside our group we could still use it as a transaction system for our small group. So from the perspective of a small group instead of an isolated individual Bitcoin seems to be a Type B asset.

ReplyDeletebitcoin is digital gold type B asset

ReplyDeletePlease let me know when BTC will go to zero $ ?? any timeframe ?? i want to buy on zero $. Thanks.

ReplyDelete